Expert Ex-SBI SAM Br. Manager will work to transform challenge of NPA Accounts into opportunities

Try free 'NPA Chat Samadhan' App !

Reviving 'Non-Performing Asset' (NPA) Accounts of Indian industry and providing guidance on 'Debt Recovery Tribunal' (DRT) matters and complex situations under 'Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act'.

Are you tired of dealing with NPAs? Let our experienced strategic consultants help your bank or NBFC reduce and resolve NPAs efficiently.

PROFESSIONALLY EXPERT TEAM OF EX-BANKER & LAWYERS

rendering

Expert advice on NPA Resolutions, complex DRT matters and implications of SARFAESI Act

to banks and businesses, both.

NPADoctor- a Trusted brand for NPA resolution

★★★★★

Understanding the Non-Performing Assets (NPAs)

An asset is anything that is owned and has value. For banks, loans are considered assets because the interest paid on these loans is a major source of income. However, when borrowers, whether individuals or businesses, fail to pay the interest, these loans become non-performing assets (NPAs) because they stop generating income for the bank.

According to a 2007 RBI circular, an asset is considered non-performing when it stops generating income for the bank. To align with international practices, the RBI introduced a rule in 2004 that classifies an asset as non-performing if it is overdue for more than 90 days. There are different types of non-performing assets based on how long they have been overdue.

Classification of NPAs in India

Sub-Standard Assets: Loans that have been non-performing for less than 12 months.

Doubtful Assets: Loans that have been non-performing for more than 12 months.

Loss Assets: Loans that are considered uncollectible and have little value.

Example

Imagine a small business owner who takes a loan to expand their shop. Due to an economic downturn, their sales drop, and they struggle to repay the loan. If the repayment is overdue for more than 90 days, the loan becomes an NPA. The bank can then classify it as a substandard asset and take steps to recover the money, such as restructuring the loan or taking legal action.

Why NPAs Matter

High levels of NPAs can affect a bank's profitability and its ability to lend money. This can have a ripple effect on the economy, making it harder for businesses and individuals to get loans.

Steps to Reduce NPAs

Banks and financial institutions can take several measures to reduce NPAs:

Improved Credit Appraisal: Better assessment of borrowers' ability to repay loans.

Regular Monitoring: Keeping a close watch on loan accounts to detect early signs of stress.

Restructuring Loans: Offering flexible repayment options to borrowers facing temporary financial difficulties.

Legal Actions: Using legal frameworks like the SARFAESI Act to recover dues.

By understanding NPAs and taking proactive measures, banks can help maintain economic stability and support growth.

NPA Resolution & SARFAESI Act:

An Amazing Guide

For Banks & Borrowers In India

By Adv. Shakti Kumar Jain

(B.Com., CA-IIB, LL.B. Gold-medalist, Ex-SBI Officer | 35+ Years in Banking & Recovery)

Published on 31st March 2025

📌 Disclaimer: This article is for general awareness and academic purposes only. It does not constitute legal advice and should not be cited in court proceedings.

1. NPAs – What Every Businessman & Banker Must Know

What is an NPA?

👉 As a thumb rule in India, a loan turns into an NPA if continues to be irregular for 90+ days.

📊 Impact: Hurts bank profits, restricts credit flow, and triggers recovery actions.

(Illustration: Substandard → Doubtful → Loss Assets timeline)

Why Do Businesses Fall into NPAs?

Cash flow mismanagement → Unable to service debt.

Economic slowdown → Reduced sales & revenue.

Fraud/misuse → Funds diverted from business needs.

💡 Smart Move: Monitor financial health early to avoid NPA tagging.

2. How Banks Recover NPAs – Simplified

Option 1: Restructure the Loan

🔹 Bank revises terms (lower EMI, extended tenure) to help borrowers repay.

✅ Best for: Temporary cash crunch situations.

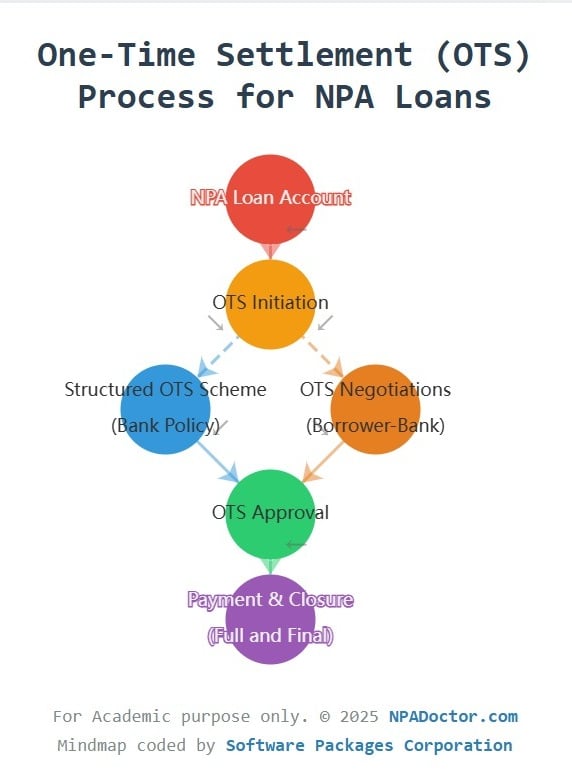

Option 2: One-Time Settlement (OTS)

OTS is a debt resolution mechanism where banks accept a lump-sum payment (typically at a discount) to close non-performing assets (NPAs). It helps borrowers avoid legal recovery while enabling banks to recover partial dues faster than litigation.

🔹 Pay a lump sum (often discounted) to close the loan.

✅ Best for: Borrowers who can arrange partial payment.

Option 3: Sell to ARCs (Asset Reconstruction Cos.)

🔹 Banks transfer NPAs to ARCs at a negotiated price.

✅ Best for: Stressed loans with low recovery chances.

Option 4: Legal Recovery (SARFAESI, DRT, IBC)

🔹 Banks seize collateral or initiate insolvency.

⚠️ Risk: Lengthy process, may not recover full dues.

3. SARFAESI Act – A Bank’s Power, A Borrower’s Nightmare

How SARFAESI Works?

1️⃣ Notice (Sec 13(2)) → 60-day warning to repay.

2️⃣ Possession (Sec 13(4)) → Bank takes collateral if unpaid.

3️⃣ Auction → Property sold to recover dues.

✔ Pay dues before auction.

✔ Prove wrongful classification.

✔ Show bank procedural lapses.

✔ An experience NPA & SARFAESI Act Resolution Consultant can Strategically help you

4. Smart Strategies for Borrowers Facing NPA/SARFAESI

For Business Owners:

Negotiate early → Better OTS deals before legal action.

Refinance debt → Shift to lower-interest lenders.

Legal recourse → Challenge wrongful notices via DRT.

For Bank Officers:

Early warning systems → Flag risky accounts before NPA.

Proactive restructuring → Prevent defaults where possible.

Transparent auctions → Maximize recovery value.

💼 Real-Life Case: A Mumbai-based builder avoided auction by negotiating an OTS within the 60-day notice period.

5. 2024 Updates – What’s New?

📌 RBI’s Stricter NPA Norms → Early warnings mandatory for high-value loans.

📌 Faster SARFAESI Process → Digital notices now valid, quicker hearings.

6. How We Can Help?

With 35+ years in SBI’s Stressed Assets Management (SAM) Branch, I assist:

🔹 Banks → High-value NPA recovery strategies.

🔹 Businesses → OTS negotiations, SARFAESI defense.

Final Word

NPAs and SARFAESI are complex but manageable with timely action & expert guidance. Whether you’re a banker managing NPAs or a businessman facing recovery, the right strategy makes all the difference.

(Illustration: Side-by-side comparison of NPA vs. SARFAESI routes)

About the Author:

Adv. Shakti Kumar Jain is a former SBO officer specializing in NPA recovery. His expertise spans banking, law, and insolvency – offering practical solutions beyond textbook theories.

(Word Count: 1,000+ | SEO-Optimized for "NPA Resolution India", "SARFAESI Consultation", etc.)

🔗 Share this with colleagues facing NPA/SARFAESI challenges!

NPA Resolution & SARFAESI Act:

An Amazing Guide

For Banks & Borrowers In India

By Adv. Shakti Kumar Jain

(B.Com., CA-IIB, LL.B. Gold-medalist, Ex-SBI Officer | 35+ Years in Banking & Recovery)

Published on 31st March 2025

📌 Disclaimer: This article is for general awareness and academic purposes only. It does not constitute legal advice and should not be cited in court proceedings.

1. NPAs – What Every Businessman & Banker Must Know

What is an NPA?

👉 As a thumb rule in India, a loan turns into an NPA if continues to be irregular for 90+ days.

📊 Impact: Hurts bank profits, restricts credit flow, and triggers recovery actions.

(Illustration: Substandard → Doubtful → Loss Assets timeline)

Why Do Businesses Fall into NPAs?

Cash flow mismanagement → Unable to service debt.

Economic slowdown → Reduced sales & revenue.

Fraud/misuse → Funds diverted from business needs.

💡 Smart Move: Monitor financial health early to avoid NPA tagging.

2. How Banks Recover NPAs – Simplified

Option 1: Restructure the Loan

🔹 Bank revises terms (lower EMI, extended tenure) to help borrowers repay.

✅ Best for: Temporary cash crunch situations.

Option 2: One-Time Settlement (OTS)

OTS is a debt resolution mechanism where banks accept a lump-sum payment (typically at a discount) to close non-performing assets (NPAs). It helps borrowers avoid legal recovery while enabling banks to recover partial dues faster than litigation.

🔹 Pay a lump sum (often discounted) to close the loan.

✅ Best for: Borrowers who can arrange partial payment.

Option 3: Sell to ARCs (Asset Reconstruction Cos.)

🔹 Banks transfer NPAs to ARCs at a negotiated price.

✅ Best for: Stressed loans with low recovery chances.

Option 4: Legal Recovery (SARFAESI, DRT, IBC)

🔹 Banks seize collateral or initiate insolvency.

⚠️ Risk: Lengthy process, may not recover full dues.

3. SARFAESI Act – A Bank’s Power, A Borrower’s Nightmare

How SARFAESI Works?

1️⃣ Notice (Sec 13(2)) → 60-day warning to repay.

2️⃣ Possession (Sec 13(4)) → Bank takes collateral if unpaid.

3️⃣ Auction → Property sold to recover dues.

✔ Pay dues before auction.

✔ Prove wrongful classification.

✔ Show bank procedural lapses.

✔ An experience NPA & SARFAESI Act Resolution Consultant can Strategically help you

4. Smart Strategies for Borrowers Facing NPA/SARFAESI

For Business Owners:

Negotiate early → Better OTS deals before legal action.

Refinance debt → Shift to lower-interest lenders.

Legal recourse → Challenge wrongful notices via DRT.

For Bank Officers:

Early warning systems → Flag risky accounts before NPA.

Proactive restructuring → Prevent defaults where possible.

Transparent auctions → Maximize recovery value.

💼 Real-Life Case: A Mumbai-based builder avoided auction by negotiating an OTS within the 60-day notice period.

5. 2024 Updates – What’s New?

📌 RBI’s Stricter NPA Norms → Early warnings mandatory for high-value loans.

📌 Faster SARFAESI Process → Digital notices now valid, quicker hearings.

6. How We Can Help?

With 35+ years in SBI’s Stressed Assets Management (SAM) Branch, I assist:

🔹 Banks → High-value NPA recovery strategies.

🔹 Businesses → OTS negotiations, SARFAESI defense.

Final Word

NPAs and SARFAESI are complex but manageable with timely action & expert guidance. Whether you’re a banker managing NPAs or a businessman facing recovery, the right strategy makes all the difference.

(Illustration: Side-by-side comparison of NPA vs. SARFAESI routes)

About the Author:

Adv. Shakti Kumar Jain is a former SBO officer specializing in NPA recovery. His expertise spans banking, law, and insolvency – offering practical solutions beyond textbook theories.

(Word Count: 1,000+ | SEO-Optimized for "NPA Resolution India", "SARFAESI Consultation", etc.)

🔗 Share this with colleagues facing NPA/SARFAESI challenges!

By Adv. Shakti Kumar Jain

(B.Com., CA-IIB, LL.B. Gold-medalist, Ex-SBI Officer | 35+ Years in Banking & Recovery)

Published on 31st March 2025

📌 Disclaimer: This article is for general awareness and academic purposes only. It does not constitute legal advice and should not be cited in court proceedings.

1. NPAs – What Every Businessman & Banker Must Know

What is an NPA?

👉 As a thumb rule in India, a loan turns into an NPA if continues to be irregular for 90+ days.

📊 Impact: Hurts bank profits, restricts credit flow, and triggers recovery actions.

(Illustration: Substandard → Doubtful → Loss Assets timeline)

Why Do Businesses Fall into NPAs?

Cash flow mismanagement → Unable to service debt.

Economic slowdown → Reduced sales & revenue.

Fraud/misuse → Funds diverted from business needs.

💡 Smart Move: Monitor financial health early to avoid NPA tagging.

2. How Banks Recover NPAs – Simplified

Option 1: Restructure the Loan

🔹 Bank revises terms (lower EMI, extended tenure) to help borrowers repay.

✅ Best for: Temporary cash crunch situations.

Option 2: One-Time Settlement (OTS)

OTS is a debt resolution mechanism where banks accept a lump-sum payment (typically at a discount) to close non-performing assets (NPAs). It helps borrowers avoid legal recovery while enabling banks to recover partial dues faster than litigation.

🔹 Pay a lump sum (often discounted) to close the loan.

✅ Best for: Borrowers who can arrange partial payment.

Illustration:

In a busy rice factory in Punjab, a Rs.260 crore loan became an NPA when sales dropped. The bank threatened to take everything under the SARFAESI Act. Then, a smart NPA resolution expert stepped in. They talked to the bank and made a deal: a One Time Settlement (OTS) for just Rs.160 crore. The factory survived, jobs stayed, and hope returned. This shows how the right knowledge of DRT rules and borrower rights can turn things around in North India. If your business faces similar trouble, the right help could make all the difference.

Option 3: Sell to ARCs (Asset Reconstruction Cos.)

🔹 Banks transfer NPAs to ARCs at a negotiated price.

✅ Best for: Stressed loans with low recovery chances.

Option 4: Legal Recovery (SARFAESI, DRT, IBC)

🔹 Banks seize collateral or initiate insolvency.

⚠️ Risk: Lengthy process, may not recover full dues.

3. SARFAESI Act – A Bank’s Power, A Borrower’s Nightmare

How SARFAESI Works?

1️⃣ Notice (Sec 13(2)) → 60-day warning to repay.

2️⃣ Possession (Sec 13(4)) → Bank takes collateral if unpaid.

3️⃣ Auction → Property sold to recover dues.

✔ Pay dues before auction.

✔ Prove wrongful classification.

✔ Show bank procedural lapses.

✔ An experience NPA & SARFAESI Act Resolution Consultant can Strategically help you

4. Smart Strategies for Borrowers Facing NPA/SARFAESI

For Business Owners:

Negotiate early → Better OTS deals before legal action.

Refinance debt → Shift to lower-interest lenders.

Legal recourse → Challenge wrongful notices via DRT.

For Bank Officers:

Early warning systems → Flag risky accounts before NPA.

Proactive restructuring → Prevent defaults where possible.

Transparent auctions → Maximize recovery value.

💼 Real-Life Case: A Mumbai-based builder avoided auction by negotiating an OTS within the 60-day notice period.

5. 2024 Updates – What’s New?

📌 RBI’s Stricter NPA Norms → Early warnings mandatory for high-value loans.

📌 Faster SARFAESI Process → Digital notices now valid, quicker hearings.

6. How We Can Help?

With 35+ years in SBI’s Stressed Assets Management (SAM) Branch, I assist:

🔹 Banks → High-value NPA recovery strategies.

🔹 Businesses → OTS negotiations, SARFAESI defense.

Final Word

NPAs and SARFAESI are complex but manageable with timely action & expert guidance. Whether you’re a banker managing NPAs or a businessman facing recovery, the right strategy makes all the difference.

(Illustration: Side-by-side comparison of NPA vs. SARFAESI routes)

About the Author:

Adv. Shakti Kumar Jain is a former SBO officer specializing in NPA recovery. His expertise spans banking, law, and insolvency – offering practical solutions beyond textbook theories.

(Word Count: 1,000+ | SEO-Optimized for "NPA Resolution India", "SARFAESI Consultation", etc.)

🔗 Share this with colleagues facing NPA/SARFAESI challenges!

NPA Resolution & SARFAESI Act:

An Amazing Guide

For Banks & Borrowers In India

By Adv. Shakti Kumar Jain

(B.Com., CA-IIB, LL.B. Gold-medalist, Ex-SBI Officer | 35+ Years in Banking & Recovery)

Published on 31st March 2025

📌 Disclaimer: This article is for general awareness and academic purposes only. It does not constitute legal advice and should not be cited in court proceedings.

1. NPAs – What Every Businessman & Banker Must Know

What is an NPA?

👉 As a thumb rule in India, a loan turns into an NPA if continues to be irregular for 90+ days.

📊 Impact: Hurts bank profits, restricts credit flow, and triggers recovery actions.

(Illustration: Substandard → Doubtful → Loss Assets timeline)

Why Do Businesses Fall into NPAs?

Cash flow mismanagement → Unable to service debt.

Economic slowdown → Reduced sales & revenue.

Fraud/misuse → Funds diverted from business needs.

💡 Smart Move: Monitor financial health early to avoid NPA tagging.

2. How Banks Recover NPAs – Simplified

Option 1: Restructure the Loan

🔹 Bank revises terms (lower EMI, extended tenure) to help borrowers repay.

✅ Best for: Temporary cash crunch situations.

Option 2: One-Time Settlement (OTS)

OTS is a debt resolution mechanism where banks accept a lump-sum payment (typically at a discount) to close non-performing assets (NPAs). It helps borrowers avoid legal recovery while enabling banks to recover partial dues faster than litigation.

🔹 Pay a lump sum (often discounted) to close the loan.

✅ Best for: Borrowers who can arrange partial payment.

Option 3: Sell to ARCs (Asset Reconstruction Cos.)

🔹 Banks transfer NPAs to ARCs at a negotiated price.

✅ Best for: Stressed loans with low recovery chances.

Option 4: Legal Recovery (SARFAESI, DRT, IBC)

🔹 Banks seize collateral or initiate insolvency.

⚠️ Risk: Lengthy process, may not recover full dues.

3. SARFAESI Act – A Bank’s Power, A Borrower’s Nightmare

How SARFAESI Works?

1️⃣ Notice (Sec 13(2)) → 60-day warning to repay.

2️⃣ Possession (Sec 13(4)) → Bank takes collateral if unpaid.

3️⃣ Auction → Property sold to recover dues.

✔ Pay dues before auction.

✔ Prove wrongful classification.

✔ Show bank procedural lapses.

✔ An experience NPA & SARFAESI Act Resolution Consultant can Strategically help you

4. Smart Strategies for Borrowers Facing NPA/SARFAESI

For Business Owners:

Negotiate early → Better OTS deals before legal action.

Refinance debt → Shift to lower-interest lenders.

Legal recourse → Challenge wrongful notices via DRT.

For Bank Officers:

Early warning systems → Flag risky accounts before NPA.

Proactive restructuring → Prevent defaults where possible.

Transparent auctions → Maximize recovery value.

💼 Real-Life Case: A Mumbai-based builder avoided auction by negotiating an OTS within the 60-day notice period.

5. 2024 Updates – What’s New?

📌 RBI’s Stricter NPA Norms → Early warnings mandatory for high-value loans.

📌 Faster SARFAESI Process → Digital notices now valid, quicker hearings.

6. How We Can Help?

With 35+ years in SBI’s Stressed Assets Management (SAM) Branch, I assist:

🔹 Banks → High-value NPA recovery strategies.

🔹 Businesses → OTS negotiations, SARFAESI defense.

Final Word

NPAs and SARFAESI are complex but manageable with timely action & expert guidance. Whether you’re a banker managing NPAs or a businessman facing recovery, the right strategy makes all the difference.

(Illustration: Side-by-side comparison of NPA vs. SARFAESI routes)

About the Author:

Adv. Shakti Kumar Jain is a former SBO officer specializing in NPA recovery. His expertise spans banking, law, and insolvency – offering practical solutions beyond textbook theories.

(Word Count: 1,000+ | SEO-Optimized for "NPA Resolution India", "SARFAESI Consultation", etc.)

🔗 Share this with colleagues facing NPA/SARFAESI challenges!

Are you struggling with Non-Performing Assets (NPA Accounts), overwhelming debt, or legal challenges under the SARFAESI Act? At NPADoctor.com, we specialize in resolving complex financial issues for both sides, borrowers and banks.

With a team of expert lawyers, Recovery procedure expert ex-Bankers and financial advisors, we provide tailored solutions for:

NPA Account Resolution

Loan Settlement

Debt Recovery Tribunal (DRT) Cases

SARFAESI Act Compliance

Whether you’re an individual seeking relief from debt or a bank aiming for efficient recovery, we’re here to help you achieve your goals.

Why Choose NPADoctor?

Expertise: Decades of experience in financial and legal solutions.

Tailored Strategies: Customized plans to meet your unique needs.

Transparency: Clear communication with no hidden fees.

Proven Results: Trusted by countless clients for successful resolutions.

Our Services:

For Borrowers

Resolve NPA Accounts and reduce financial stress.

Negotiate loan settlements to lower your debt burden.

Navigate Sarfaesi Act challenges with expert legal support.

For Banks

Efficiently recover assets through DRT and SARFAESI Act processes.

Streamline NPA resolutions with professional guidance.

Take the First Step Toward Financial Freedom

Don’t let financial challenges hold you back. Whether you’re a borrower or a bank, NPADoctor.com is here to help you achieve clarity, stability, and success.

Why Wait? Let’s Get Started !

To ensure high-quality tailor-made service to clients, we allow only very limited and high Value NPA Accounts to enroll for our services. To avoid disappointment, contact us today to schedule a consultation and discover how we can help you reclaim your financial future.

Case Study: Turning Financial Struggles into Success

Client Profile*

Name: Mr. Rajesh Kumar

Industry: Manufacturing

Challenge: Struggling with

an NPA account of ₹2 crores

and facing asset seizure under

the Sarfaesi Act.

The Problem

Mr. Kumar’s manufacturing business was hit hard by the pandemic, leading to cash flow issues and an inability to repay loans. His account was declared an NPA, and the bank initiated asset recovery under the SARFAESI Act.

The Solution

NPADoctor.com stepped into the scene:

Analyze the financial situation and negotiate with the bank for a loan restructuring plan.

Represent Mr. Kumar in DRT proceedings to halt asset seizure.

Provide legal guidance to ensure compliance with the SARFAESI Act.

The Result

The bank agreed to restructure the loan, reducing the monthly EMI burden.

Asset seizure was halted, allowing Mr. Kumar to continue operations.

Within 12 months, Mr. Kumar’s business was back on track, and he successfully cleared his dues.

"NPADoctor.com gave me a second chance. Their expertise and dedication saved my business and my livelihood." – Rajesh Kumar

*Client name etc., changed to protect identity.

Why Clients Trust NPADoctor.com?

Proven Results: From loan settlements to NPA resolutions, we deliver tangible outcomes.

Client-Centric Approach: We listen, understand, and tailor solutions to your unique needs.

Our lawyers and financial advisors are among the best in the industry.

Our approach is Tailor-made.

We value client's time, we take assignment of very few clients and once the appointment is scheduled, try to ensure Zero waiting time.

Top rated by 100+ clients

★★★★★

The Ultimate NPA Resolution Advice: Unlocking Your Financial

Destiny bring you here to introduce you to this unique service.

"You have not come here to stop, but to take action on top priority."

Imagine a bank struggling with rising NPAs, affecting its ability to lend and grow.

Or a borrower, overwhelmed by debt, unsure of how to navigate the financial storm.

This is where 'NPADoctor' steps in, offering expert advice and solutions to resolve NPAs and secure a stable financial future.

The NPADoctor, works for its client who engaged it, but creates 'Win Win' situation for all the stake-holders.

Discover the power of NPA resolution with our expert advice on navigating the challenging waters of financial recovery. Don't miss out on this opportunity to secure your financial future.

What is the NPA limit for the Sarfaesi Act?

The SARFAESI Act applies to loans that are classified as Non-Performing Assets (NPAs) and exceed Rs. 1 lakh. However, it does not cover loans where more than 80% of the amount has already been repaid, and it excludes certain assets such as agricultural land.

What are the methods of recovery of NPA under Sarfaesi Act?

The SARFAESI Act provides several ways to recover Non-Performing Assets (NPAs):

Securitization: Converting loans into marketable securities and selling them to investors.

Asset Reconstruction: Asset Reconstruction Companies (ARCs) buy NPAs from banks and work on recovering the dues.

Enforcement of Security Interest: Banks can take possession of the borrower's secured assets and sell them to recover the loan amount without needing court intervention.

These methods help banks manage and reduce NPAs, ensuring better financial health and stability.

Remarkable NPA Resolution Secrets for Banks, Borrowers, and Auction Purchasers

Uncover the hidden secrets of NPA resolution and gain a competitive edge in the market. Our proven techniques will help you achieve remarkable results in no time.

Our comprehensive approach includes:

Early Identification: Detect potential NPAs before they impact your financial health.

Customized Resolution Plans: Develop strategies tailored to your specific needs.

Regulatory Compliance: Navigate the complex regulatory landscape with ease.

Stakeholder Communication: Maintain transparent and effective communication with all parties involved.

By leveraging our expertise, you can achieve:

Reduced Financial Risk: Minimize the impact of NPAs on your balance sheet.

Improved Asset Quality: Enhance the overall quality of your asset portfolio.

Competitive Advantage: Stay ahead of competitors by effectively managing NPAs.

Sustainable Growth: Build a solid foundation for long-term success.

Join the ranks of successful businesses that have transformed their NPA challenges into opportunities. Contact us today to learn how our proven techniques can deliver remarkable results for your organization.

For more insights on effective NPA resolution strategies, click and explore these resources:

Strategies for Effective NPA Resolution

Resolution Strategies for Maximizing the Value of Non-Performing Assets (NPAs)

Dealing with NPAs: Lessons from International Experiences

🛠️ We Revive Your Business with Expert NPA resolution

Expertise You Can Trust: Service by Mr. Shakti Kumar Jain, an ex-SBI veteran with 35+ years of experience in banking, including 10 years prize winning specializing in Hight Value NPA resolution / hard recovery, OTS, DRT matters, SARFAESI Act implementation at ground level and more.

Unique Insights: Master of both sides—bank recovery strategies and defense for struggling companies against harsh actions.

Proven Solutions: Got many rewards for recovery of chronic bad loans during the SBI service in SAM Branch. After retirement established 'NPA Doctor' in 2015, strategically resolving numerous complex NPA loan cases and facilitating fair settlements thus helped the Banks and the sick industries both.

Legal & Procedural Excellence: Founder Mr. Shakti Kumar Jain is not only highly experienced In the field, but also an LL.B. Gold medalist as well. He is specialized in handling SARFAESI, DRT, forensic audits, criminal cases, and willful defaulter actions.

Protecting Stakeholders:

Assisting the Companies navigating in NPA Accounts financial crisis, while safeguarding the honest Bank Officers from undue harassment in court cases or in departmental vigilance accountability cases.

NPA Doctor is the ‘NPA Helpline’

It helps both, the Banks and the NPA Borrowers.

NPADoctor is your partner in turning challenges into opportunities.

Adv. Shakti Kumar Jain

B.Com., CA-IIB, LL.B. Gold medalist

Ex-Officer, SBI SAM Branch

NPADoctor Navigates complex banking challenges with precision, especially in re-circulating the funds blocked in NPA Accounts and the bloour consultancy specializes in loan recovery and dispute management, strategising and handling court matters especially in DRT and in NCLT, ensuring your financial interests are protected through strategic legal and financial interventions.

NPA Loan Recovery Strategies

Customized expert guidance on navigating non-performing assets and revitalizing your financial standing through effective solutions.

Struggling with a Non-Performing Asset (NPA) Account?

Don't Lose Hope!

Facing a loan default can be stressful, but there are options. NPADoctor simplifies legal complexities surrounding NPAs and the way outs to resolve it.

NPADoctor is a Trusted brand for NPA Resolution

★★★★★

We provide expert legal and strategic advice on

the possibilities for rephasement or re-structuring of loan,

reaching the compromised OTS in NPA Accounts,

and an amicable settlement of disputes or mis-understandings

between the Banks and its client(s),

settlement of NPA Loans,

filing on behalf of Banks or defending on behalf or borrowers or guarantors,

the OA (recovery suits) or SA (Securitization Application) in DRT,

and the Matters in NCLT or in High Court,

declaration of non-cooperative borrower or willful defaulter,

fraud investigation, complaint to police, EoW or ACB in CBI.

★★★★★

Our advisory services cater to banks, NBFCs, borrowers, guarantors, and all parties involved in SARFAESI auctions.

NPADoctor is a Trusted brand for NPA Resolution

Determine Residence Status under Indian Income Tax Act

The Table is meant only for easy academic understanding the concept of Resident/NOR/NRI under Indian Income Tax Act, Please consult with professional for serious usage

The Table presents a proper view on Desktop or Laptop

NPADoctor transformed our loan recovery process with their expert legal and financial solutions. Highly recommended!

Audi Yadul*

Industrialist

Their insider banking knowledge helped us navigate complex disputes effectively. We are extremely satisfied with the results!

Renu Singla* Banker

* Actual identity changed for privacy and security

NPADoctor is a Trusted brand for NPA Resolution

★★★★★

* Actual identity changed for privacy and security

★★★★★

How we help you

Unlock the expert legal and financial solutions for NPA accounts, loan recovery, and settlement.

Led by ex-Banker turned lawyer,

Adv. Shakti Kumar Jain,

our firm ensures precision, integrity,

and client-focused strategies.

Explore our services and discover how we can assist you in navigating complex legal landscapes with confidence.

Consult us

© 2015 npadoctor.com

All rights reserved.

Created with ❤️ by Klick

IMPORTANT NOTICE

The information provided on this website is for academic and general awareness purposes, and, we, in no way solicit to invite clients or to promote our services.

Though, every effort has been made to provide accurate information a the time of posting the same, yet no responsibility, what so ever it may be is assumed by the owner, publisher or the blog writer etc. persons connected with this website.

We advise you to consult lawyers and subject professionals for your matters.

The information provided is not meant for production in Court Cases.